Global container trade has now recovered and surpassed pre-COVID levels.

Extremes in freight demand across the various regions are distorting container supply.

Increased demand, combined with supply chain bottlenecks, have led to extended container cycle times, reducing capacity, and increasing rates.

Whilst global trade volumes are mostly stagnant, the Indian subcontinent and Middle East have seen a significant decline in trade versus 2019.

On the other hand, North America is experiencing a boom in demand, with import volumes showing extraordinary growth.

North American imports are up 40% year-on-year and up 10% over the last two years, driven by surging demand for high volume consumer goods.

The result of this misalignment has created massive bottlenecks, absorbing container capacity and putting not only ports but inland logistics under immense pressure.

North America is supposedly responsible for around 55-60% of the structural deficit of equipment in the Far East.

This is largely due to increased demand, chassis shortages, port congestion and supply chain bottlenecks in the US.

A significant volume of equipment is stuck in inland depots.

High levels of rollover and transhipments are leading to extended transit times.

Schedule reliability is also at an all-time low, with space/equipment going to highest bidder and many long-term contracts not being fulfilled by lines.

Port Congestion and Labour Shortages Cause Further Trouble

Port congestion and labour shortages have made it more difficult to reposition empty container.

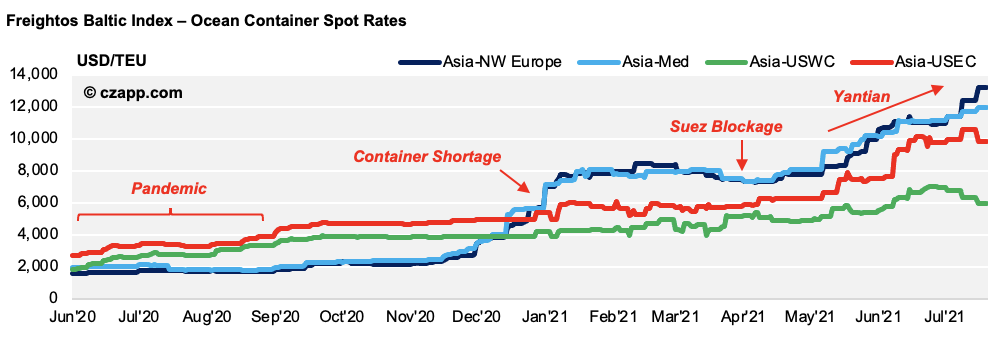

After a month-long cut in productivity due to COVID, Yantian port in Shenzhen (Southern China) resumed normal operations on the 24th June.

Although operational capacity at Yantian had steadily recovered through June, we think it’ll still take more than two months to clear the backlog of more than 700,000 TEU.

The probability for further localised disruption remains high across many areas in Asia.

Borders between Myanmar and China have recently tightened due to another wave of COVID cases, although little impact is expected on legitimate trade flows.

The Threat of Increased Regulation

The container shipping sector has consolidated over the past few years.

A drive to consolidate saw the formation of key shipping alliances encompassing more than 80% of the market.

APM-Maersk and Mediterranean Shipping Company, or MSC, joined the 2M pact; CMA CGM, Cosco and Evergreen formed the Ocean Alliance, whilst others including Hapag Lloyd, ONE and Yang Ming created THE alliance.

Financial reports show all major carriers posting record profits in Q1’21, with operating profits ranging from 500-970 USD/TEU.

Incredibly, HMM recorded the highest operating profit of nearly 1000 USD/TEU shipped.

A TEU container ship (Twenty-Foot Equivalent Unit)

Whilst lines continue to implement blank sailings in an effort to restore services, blank sailings further reduce capacity, pushing up rates.

On the 9th July, President Biden issued an executive order calling on regulators to tackle the issue of high shipping costs and unreasonable surcharges.

Transportation bottlenecks and sky-high costs are severely impacting US exporters and have driven US inflation to a 13-year high.

Across the US, prices of food items and consumer goods have soared, and stock shortages are already occurring in some sectors.

Other nations, including China, Vietnam and South Korea, have also attempted to tackle high shipping costs over the past year with little to no impact.

Market Outlook

The fight for Trans-Pacific vessel space should intensify through July and August as we enter peak shipping season and US retail activity surges.

The backlog in US-bound cargo built up during the recent COVID-19 outbreak in China should also arrive on the US West Coast, exacerbating port congestion.

Freight rates could remain strong until 2023, with pricing unlikely returning to 2011-2019 levels in that time, if ever again.

Lines should continue to use capacity management to maintain strong rate levels, but the current supply chain challenges/demands have supported their strategies.

As lines return to profitability, they’ve invested heavily in their new vessel order books.

However, new vessel deployment won’t be until 2024 at the earliest.

We ultimately think rates find a middle ground between current and 2018/19 levels in that near-term period.