This article was first published on czapp.com, Czarnikow’s market portal that provides you with get daily market intelligence on agricultural and energy commodities.

Insight Focus

Demand for Chinese PET resin should drop with two of the key buyers at war.

Prices will likely leap as Brent crude oil breaches 100 USD/bbl.

European PET resin prices should also climb as energy and raw material costs rally.

War in Ukraine Hits International PET Flows

Russia’s invasion has hit all commodity markets, with PET resin no exception.

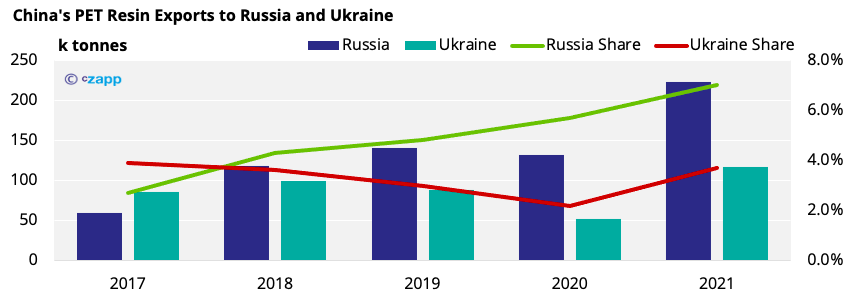

Both Russia and Ukraine are key markets for China, with Russia the main buyer of Chinese PET resin.

Over the last five years, Russia’s offtake has jumped from around 60k tonnes in 2017 to nearly 225k tonnes in 2021, representing over 7% of China’s total PET resin exports.

However, the Rouble has hit a record low against the Dollar following last week’s attack on Ukraine, and it’ll likely come under sustained pressure as Europe and the US strengthen economic sanctions.

Russia’s demand for USD-denominated Chinese PET exports should therefore be hit, causing a ripple effect across Asian markets.

Although Russia’s PET market is largely self-sufficient, domestic PET contracts are typically formula linked to USD-denominated Chinese PET prices.

As a result, Russian bottlers and converters will be hit by a substantial inflation shock, lowering future import requirements.

As for Ukraine, it has traditionally been a key buyer of Chinese PET, although China’s lost market share to Lithuania in recent years.

Having said that, Europe’s production constraints and outages saw China’s exports to Ukraine rebound to an all-time high (∼166kmt) in 2021.

Whilst loss of Ukrainian demand in isolation would have a limited impact on China’s total export flows, further expansion of the conflict zone could weaken China’s access to the wider region.

Shippers are already reporting disruption of flows into the Black Sea, but the situation remains fluid and is changing by the hour.

According to Hellenic Shipping News, all Ukrainian commercial ports have reportedly stopped operations, including the main port of Odessa.

The Russian Navy has also restricted access to the Kerch Strait and the north-western part of the Black Sea, impacting all Ukrainian ports east of Crimea, including Mariupol.

Petrochemical Prices Jump as Crude Breaches 100 USD/bbl

Russia’s invasion has also sent Brent crude oil prices soaring, touching 105 USD/bbl last week for the first time since 2014.

Russia is the second-largest exporter of crude oil, after Saudi Arabia, and is also the world’s largest natural gas exporter, accounting for 35% of Europe’s supply.

Crude prices eased on Friday as Russia’s energy industry avoided sanctions.

It then opened 5% higher on Sunday and looks set to remain above 100 USD/bbl in the near term.

Given Europe’s integrated and deep-set reliance on Russian energy resources, any ban on crude or gas exports would have severe and mutually assured economic repercussions.

Global commodities and petrochemical prices jumped following the surge in crude.

Olefin and aromatics, key petrochemical feedstocks for plastic production, saw prices leap in major markets.

PTA futures immediately reacted, tracking crude oil closely as we would expect.

However, in the past few days, we’ve seen good selling pushing futures downward.

Whilst, in Europe, PX and PTA spot prices also saw sharp increases, with PX spot prices up 45 USD/mt on the week.

European Energy Costs Increase

Alongside increasing raw materials, the Dutch Natural Gas contract, a leading European gas benchmark, increased by as much as 62% on news of invasion last Thursday.

German power for March increased by as much as 58%.

Although European gas prices eased on Friday, they regained upward momentum on Monday and remain close to record levels.

The impact of higher energy costs will result in increased production costs for European PET producers.

However, unlike last year, most PET producers have structured new 2022 contracts to include a range of variable components.

A new wave of surcharges is therefore not expected at this stage.

Market Implications & Concluding Thoughts

The situation is fluid and highly volatile.

However, fallout from the conflict looks set to weaken China’s PET export demand and producer margins, making it difficult to sustain current levels into H2’22.

Further freight disruption may also stimulate rate increases, leading to higher landed costs in key markets, compounding European supply constraints.

Within Europe, increased energy costs and increases in raw material prices will result in higher PET resin contract prices.

European spot PET prices should rise into March following higher import parity levels and increased pre-peak season buying.

For more analysis like this sign up to Czapp for free. If you found this content useful, share it on Facebook, Linkedin and Twitter.